Author’s Note: This article was originally created for Artemis Research and is intended for informational purposes only, not as a trade recommendation. I apologise for not cross-posting earlier - it has already been posted on my Twitter as an Article. Again, this is a research report only, and should be taken as such.

This piece thus only serves to inform, not to advice. I hope you enjoyed the time & effort I put into this. I hold positions in the assets mentioned in this article.

Original Piece: https://www.artemis.xyz/research/raydium-king-of-solana-de-fi

~ 0xKyle

DISCLAIMER: This document is provided for informational purposes only and does not constitute financial, investment, or legal advice. The content is based on sources believed to be reliable; however, no guarantee is made regarding its accuracy, completeness, or timeliness. Any reliance on this information is at your own risk.

The author(s) may hold positions in, and may buy or sell, assets or securities mentioned at any time without notice. This document may contain forward-looking statements that involve risks and uncertainties; actual results may differ materially. Past performance is not indicative of future results.

It is essential to consult with a qualified financial advisor to assess the risks and suitability of any investment decisions. The author(s) disclaim any liability for direct, indirect, or consequential loss or damage arising from the use of this document. By accessing this document, you agree to these terms.

Overview

The 2024 cycle has seen the dominance of Solana thus far, with the major narrative of this cycle - Memecoins, all spawning on Solana. Solana is also the best-performing Layer 1 blockchain in terms of price appreciation, with it being up ~+680% YTD. While memecoins and Solana are deeply intertwined, Solana has generally seen renewed interest as an ecosystem since its resurgence in 2023, with its ecosystem booming - protocols like Drift (Perp-DEX), Jito (Liquid Staking), Jupiter (DEX-Aggregator) all having tokens with billion dollar valuations, Solana active addresses and number of daily transactions eclipsing all other chains.

At the heart of this thriving ecosystem is Raydium, Solana's premier DEX. The old adage “In a gold rush, sell shovels” perfectly captures Raydium’s position: while memecoins draw the spotlight, Raydium quietly powers the liquidity and trading that fuel this activity. Benefiting from the constant flow of memecoin trading and broader DeFi activity, Raydium has solidified itself as a piece of crucial infrastructure within Solana’s ecosystem.

Here at Artemis, we believe in an increasingly fundamentally driven world - as such, the purpose of this paper is to build a fundamental paper that highlights Raydium’s place in Solana’s ecosystem. Using a data-driven approach, we aim to break down Raydium’s place in the Solana ecosystem with a first-principles approach. Let’s dive right in:

A Brief Introduction To Raydium

Launched in 2021, Raydium is an automated market maker (AMM) built on Solana, enabling permissionless pool creation, lightning-fast trades, and ways to earn yield. The key differentiating factor about Raydium lies in its structure - Raydium was the first AMM on Solana, and launched the first orderbook-compatible hybrid AMM in DeFi.

When Raydium launched, they utilized a hybrid AMM model that allowed idle pool liquidity to be shared with central limit order books, while at that time usual DEXs could only access liquidity within their own pools. This meant that liquidity on Raydium also created a market on OpenBook that was tradable on any OpenBook DEX GUI,

While this was the major differentiator in the early days, the feature has since been turned off due to an influx of predominantly long-tail markets. Raydium currently offers three different type of pools, namely:

Standard AMM Pools (AMM v4), formally known as the Hybrid AMM

Constant Product Swap Pools (CPMM), with Token 2022 support

Concentrated Liquidity Pools (CLMM)

For every swap that occurs on Raydium, a small fee is charged depending on the specific pool type and pool fee tier. This fee is split and goes to incentivizing liquidity providers, RAY buybacks, and the treasury.

Below we’ve documented the trading fees, pool creation fees and protocol fees of the different pools on Raydium. Here’s a quick breakdown of what each of the terms mean, and their respective fee levels:

Trading fees are the fees charged to traders on a swap

Buyback fees are a percentage of trading fees taken to buy back the Raydium token

Treasury fees are a percentage of trading fees allocated to the treasury

Pool creation fees are fees levied upon creation of pools, meant to deter pool spamming. Pool creation fees are controlled by the protocol multisig and reserved for protocol infrastructure costs.

The DEX Landscape On Solana

Now that we’ve managed to break down how Raydium works, we’ll be moving on to assessing Raydium’s position in the Solana DEX landscape. It goes without saying that Solana has managed to climb the ranks amongst L1s in the 2024 cycle - putting Ethereum aside, Solana is the chain with the 3rd most TVL, directly behind Tron (2nd) and Ethereum (1st).

Solana continues dominating in metrics relating to user activity, such as Daily Active Addresses, Daily Transactions, and DEX trading volumes. This rise in activity and monetary liquidity on Solana can be attributed to a couple of different factors, with the one of the more famous ones being the “memecoin frenzy” on Solana. Solana’s high speed and low cost in settlement, combined with its slick user experience for D-Apps has led to the growth and flourishing of on-chain trading. With tokens like $BONK and $WIF that have reached multi-billion dollar market-caps and the emergence of Pump.fun, a memecoin launchpad, Solana has become the de-facto home of memecoin trading.

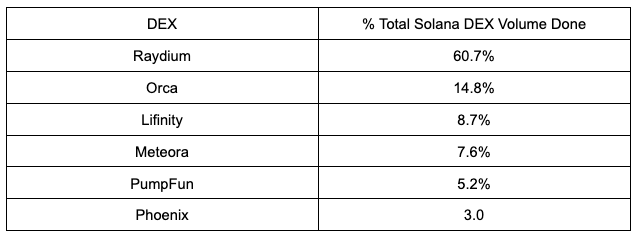

Solana has been, by far, the most used Layer 1 this cycle, and continues to dominate amongst the other L1 in terms of trading activity. As direct beneficiaries of increased activity, this means that DEXes on Solana have been doing extremely well - more traders means more fees, which means more revenue to the protocol. However, even amongst the DEXes, Raydium has managed to capture considerable market-share, as shown in the data below:

Today, Raydium ranks 1st amongst the other Solana DEXes, doing the most volume out of every one of them. Raydium dominates 60.7% of total Solana DEX volume - and this is because Raydium allows all sorts of activity to be done on them - from memecoins, to stablecoins.

One way Raydium does this is by offering pool creators and liquidity providers several choices when creating a new market. Users can opt for constant product pools for price discovery on initial launch or choose to LP in tighter ranges on concentrated liquidity pools -- allowing initial price discovery to happen on Raydium for long-tail assets and while still remaining competitive on SOL-USDC, Stablecoin, LST and other markets.

On top of that, Raydium continues to be the most liquid DEX to trade on. It’s important to note that DEXes are often an economies of scale problem, as traders flock to the exchange with the most liquidity to avoid slippage on their trades. Liquidity begets liquidity - and it becomes a positive flywheel as the largest DEX gets the most traders, which attracts liquidity providers for them to make money off of fees, which attracts more traders who yearn to avoid slippage - the cycle continues.

Liquidity is often an underlooked factor when comparing DEXes, but it’s crucial in evaluating the best-performer - especially considering that traders on Solana are trading memecoins which - on top of being extremely illiquid, require a schelling point to converge around - fragmentation of liquidity across DEXes would result in poor user experience and general dissatisfaction to buy different memecoins across DEXes every time.

Examining The Relationship Between Memecoins & Raydium

Raydium’s popularity can also be attributed to the resurgence of memecoins on Solana, especially by PumpFun, a memecoin launchpad that has made over $100mm in fees since inception earlier this year.

PumpFun memecoins have a direct line to Raydium - when a token launched on Pump.fun reaches a market cap of $69,000, Pump.fun automatically deposits $12,000 worth of liquidity into Raydium. Continuing on the earlier point regarding liquidity, this means that Raydium is, de-facto, the most liquid platform to trade memecoins on. Like a virtuous cycle, pump.fun bonds to Raydium > memecoins launch there > people trade there > it gets liquidity > more memecoins launch there > it gets more liquidity, and the cycle repeats.

Thus, Power Law has been attributed to Raydium, where virtually >90% of PumpFun generated memecoins do their business on Raydium. Like a mall in a city, Raydium is the largest “mall” on Solana, meaning that most people go to Raydium to do their “shopping”, and most “businesses” (tokens) want to set up shop there.

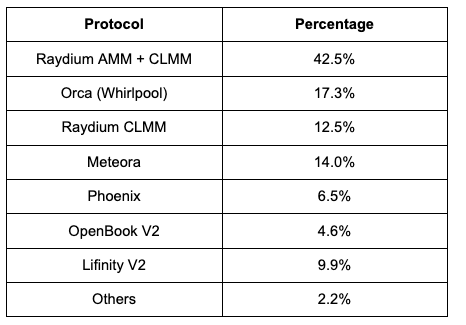

However, it’s important to note that while PumpFun relies on Raydium, the opposite isn’t true - Raydium doesn’t actively rely only on memecoins for their volume. In fact, according to Figure 8, the top 3 largest volume traded pairs in the last 30 days are SOL-USDT/USDC, contributing to more than 50% of all volume. (Note: The two SOL-USDC pairs are two different pools with different fee structures).

Figure 7 and Figure 9 also serve to substantiate this, with Figure 7 showing that SOL-USDC far outclasses all other DEX pairs in terms of volume. Figure 7 represents volumes across all all DEXes, it still goes to show that volumes across the ecosystem aren’t necessarily only driven by memecoins. Figure 9 goes one step further to show Raydium volume by token type, and we can see that “native” takes up the largest market share, at over 70%. As such, while memecoins are substantial parts of Raydium, they don’t necessarily make up the whole picture.

That being said, memecoins are highly volatile, and volatile pools usually have larger fees - as such, while memecoins may not contribute as much as the Solana pools volume wise, they are a large contributor to revenue and fees for Raydium. This is evidenced in looking at the month of September - because memecoins are such cyclical assets, during “bad markets”, they tend to underperform greatly as risk appetite diminishes. Revenues for PumpFun subsequently dropped 67% from an average of $800k a day in July / August, to around $350k a day in September; We saw the same drop in fees for Raydium during that time period;

But like everything else in crypto, this industry is highly cyclical, and it’s normal to see a drop in metrics during bear markets as risk washes out. Instead, we can focus at TVL as a measure of the true anti-fragility of the protocol - while revenues are highly cyclical and come and go with the arrival / departure of speculators, TVL is a metric that stands to signify the sustainability of a DEX, and how it stands the test of time. TVL is similar to the “occupancy” of a mall - while fads come and go, and the mall usage may vary according to seasonality just like in reality, as long as the mall has an above average occupancy, we can gauge its success.

And similar to a well-packed mall, Raydium has consistent TVL over-time, signifying that while its revenues may fluctuate with market prices and sentiment, it has demonstrated its ability to be a main-stay product of the Solana ecosystem, and to be the best and most liquid DEX on Solana. Thus, while memecoins do contribute in-part to its revenues, volume is not always done on memecoins, and liquidity still flocks to Raydium no matter the season.

Raydium vs Aggregators

While Jupiter and Raydium don’t directly compete, Jupiter acts as the key aggregator in the Solana ecosystem, routing trades through the most efficient paths across multiple decentralized exchanges (DEXes), including Raydium. Essentially, Jupiter functions as a meta-level platform that ensures users receive the best prices by sourcing liquidity from various DEXes such as Orca, Phoenix, Raydium, and others. Raydium, on the other hand, serves as a liquidity provider, powering many of the trades Jupiter routes by offering deep liquidity pools for Solana-based tokens.

While the two protocols work hand-in-hand, it’s worth noting that the share of organic volume from Raydium directly is slowly increasing, and the share from Jupiter is slowly decreasing over time. At the same time, Raydium accounts for nearly 50% of all of Jupiter’s maker volume.

This indicates that Raydium has been successful in building a more robust, self-sustaining platform that attracts users directly, rather than relying on third-party aggregators like Jupiter.

The increase in direct volume suggests that traders are finding value in interacting with Raydium’s native interface and liquidity pools, as users seek out the most efficient and comprehensive DeFi experience without needing to go through aggregators. Ultimately, this trend highlights Raydium’s ability to stand on its own as a dominant liquidity provider in the Solana ecosystem.

Raydium vs The World

Lastly, below is a Comp Table we’ve built using the Artemis plugin for Raydium versus the other DEXes on Solana, including aggregators

In Figure 13, we compared Raydium against the most popular DEXes on SOL, namely Orca, Meteora, and Lifinity - together, the 4 of them make up 90% of Solana total DEX volume. We also included Jupiter as an aggregator. Meteora doesn’t have a token, but we still included it for the sake of comparison.

We can see that Raydium trades at the lowest MC/Fees and FDV/Fees amongst all the DEXes. Raydium also has the most number of daily active users, and all the other DEXes have more than 80% less TVL than Raydium - except for Jupiter, who we consider an aggregator and not a DEX.

And in Figure 14, we compare Raydium to other more traditional DEXes on other chains - as we can see, Raydium does more than twice of Aerodrome’s annualized DEX volume, yet trades at a lower MC/Earnings ratio.

Raydium’s Token

The tokenomics for Raydium are broken down below:

The Raydium token has multiple use-cases: owners of $RAY can stake their Raydium tokens to obtain additional $RAY. On top of that, it’s a mining reward used to attract liquidity providers to Raydium, allowing for thicker liquidity pools. Although the Raydium token is not a governance token, a governance method is in development.

While emission tokens fell out of favor with the market post-DeFi Summer, it’s worth noting that Raydium’s annual inflation rate is incredibly low, and its annualized buybacks is one of the best in DeFi. Annualized emissions are currently ~1.9mm RAY, with RAY staking accounting for 1.65m of total emissions, which is little compared to what other popular DEXes were emitting at their peak. At current prices, RAY emits around $5.1mm USD worth of RAY annually. This is very little, compared to Uniswap who, before fully unlocking, was emitting at $1.45mm USD a day, or $529.25mm USD a year.

As we recall, a small trading fee is taken for every swap in a pool on Raydium. As stated in the docs, “Depending on the specific fee of a given pool, this fee is split and goes to incentivizing liquidity providers, RAY buybacks, and to the treasury. In summary, 12% of all trading fees go to buying back RAY regardless of a given pool's fee tier.” This fact, coupled with the amount of volume Raydium does, has sparked some pretty incredible outcomes.

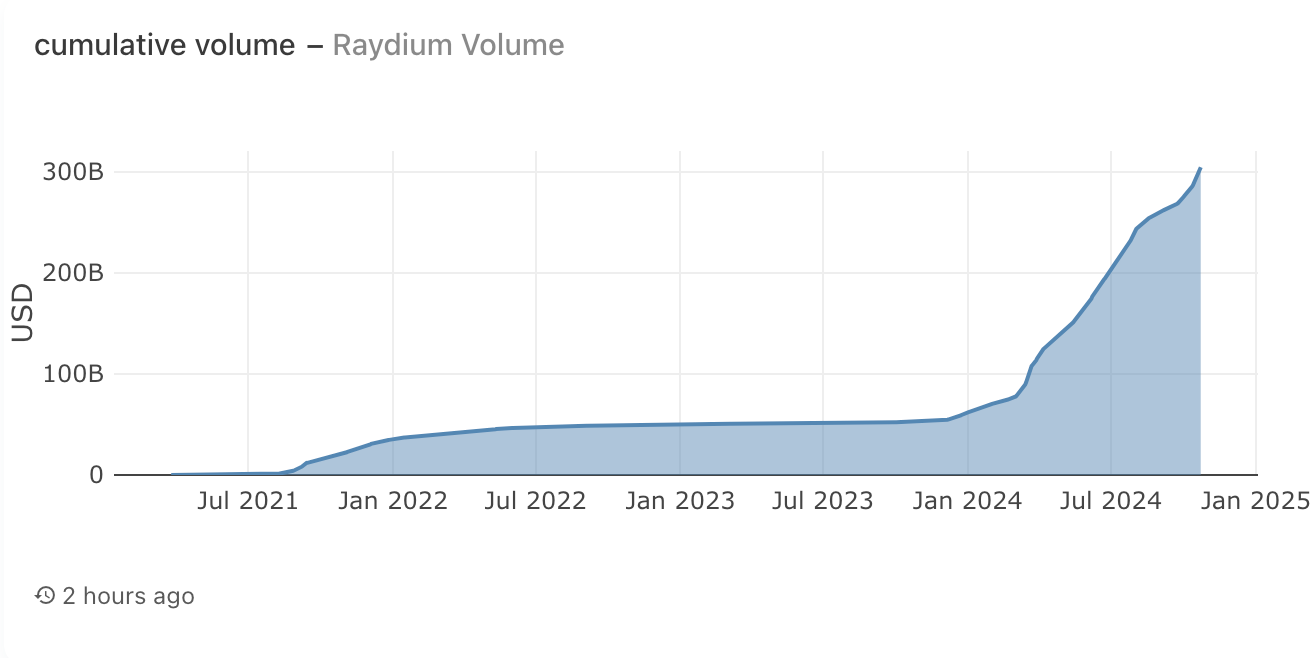

The results speak for themselves. Cumulative, with over $300Bn worth of volume done, Raydium has managed to buy back approximately 38mm RAY tokens, equivalent to $52mm USD worth. Raydium’s buyback programme is the strongest throughout all of De-Fi, and it has helped propel Raydium to the top amongst all DEXes on Solana.

The Case For Raydium

In conclusion, Raydium is fundamentally heads and shoulders above all DEXes on Solana, and is in one of the best positions to succeed with continued Solana growth. Raydium’s growth story is incredible from the past year, and it doesn’t look like it’s stopping anytime soon as memecoins continue to take dominant mindshare in crypto, with the latest memecoin craze being centered around AI (e.g $GOAT).

Raydium’s unique position as the primary liquidity provider and AMM on Solana gives it a strategic advantage in capturing market share from emerging trends. On top of that, Raydium’s commitment to innovation and ecosystem growth is reflected in its frequent upgrades, robust incentives for liquidity providers, and proactive engagement with the community. These factors suggest that Raydium is not only prepared to adapt to the evolving DeFi landscape but also to lead it.

Ultimately, Raydium acts as a piece of crucial infrastructure in one of the fastest-growing blockchain ecosystems, and if it continues on its current trajectory, it’s safe to say that the protocol seems well-positioned for growth in the future.